Know the types of banking systems in India, Indian banks and their function, RBI and more.

There are various types of banks in India and their services include accepting deposits, providing loans, issuing credit cards, facilitating transactions and offering other financial services.

The Banking System in India is an important topic for government exam preparation including UPSC, IBPS, RBI, SSC, Insurance, Defense and other state exams.

Aspirants should know about various types of banks operating in India and their functions, central banking authority (RBI) and monetary control tools.

The Reserve Bank of India (RBI) was established on 1st April, 1935. It is called the supreme monetary authority or the central banking authority.

Overview of the Banking System in India

Here is a quick overview of the types and sub-types of Indian banks.

| Types of Banks | Sub-types |

| Central Bank | – |

| Commercial Banks | Public Sector Banks Private Sector Banks Foreign Banks Regional Rural Banks |

| Co-operative Banks | State Co-operative Banks Urban Co-operative Banks |

| Small Finance Banks | – |

| Specialized Banks | – |

| Payments Banks | – |

| Scheduled Banks | – |

| Non-scheduled Banks | – |

Types of Banking System in India

The banks in India are divided into several types. Given below are the types of banks in India and their branch distribution.

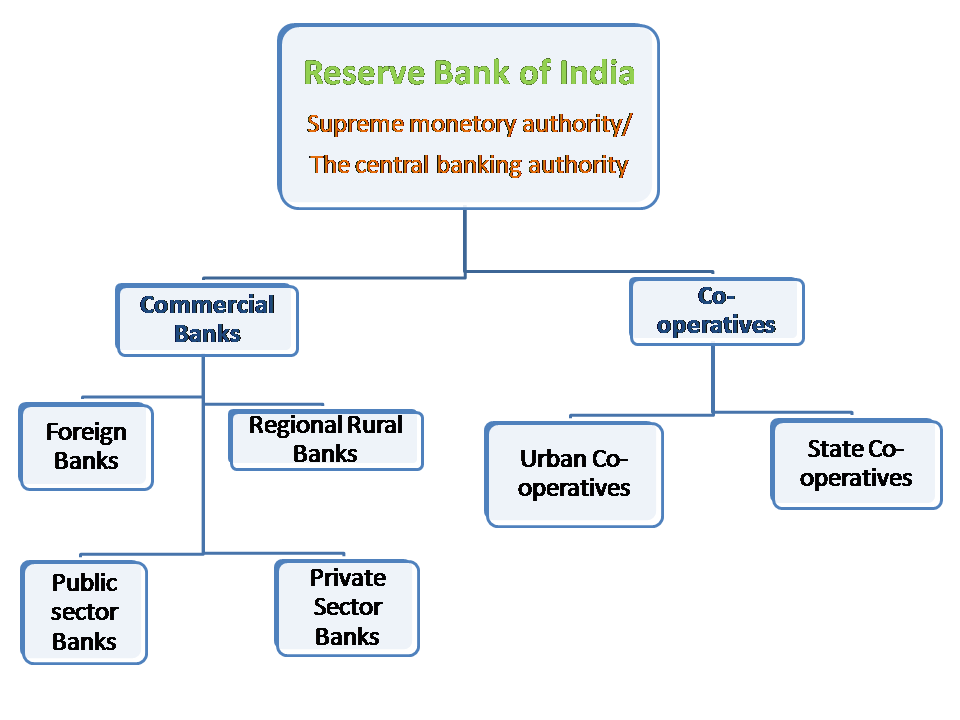

1.1

1.1: Indian Banking System

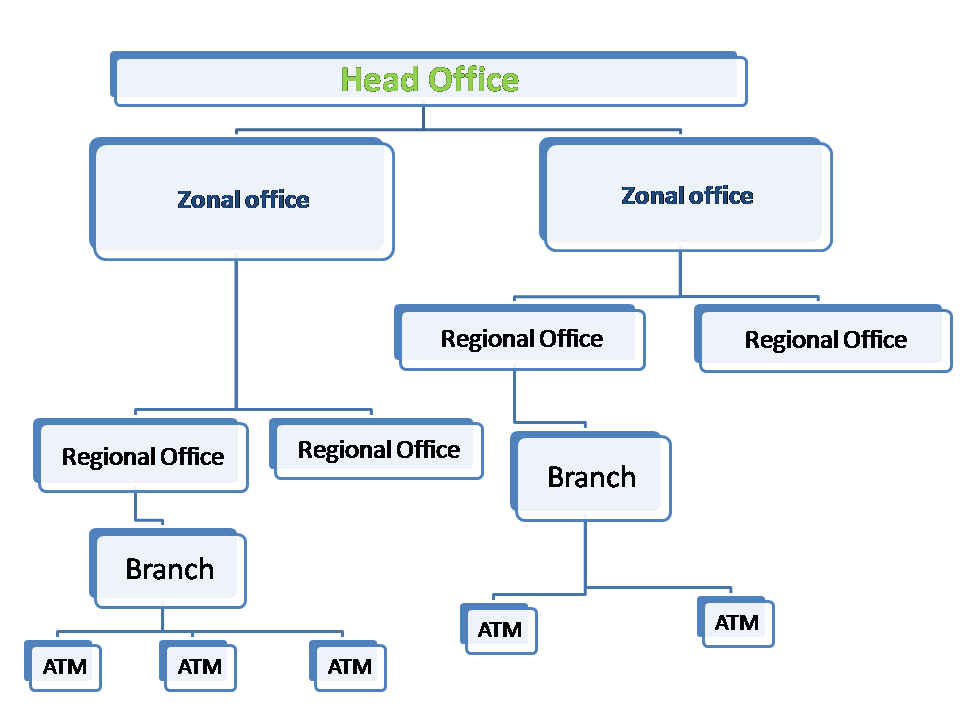

1.2

1.2: Distribution of branch

Central Bank

The Reserve Bank of India (RBI) is the central banking authority of India. It was established on 1st April 1935.

The Basic function of RBI

The basic function of RBI is to regulate the issue of bank notes and the keeping of reserves with a view to securing monetary stability in India. In simple terms; RBI is aware of operating the currency and credit system of the country to its advantage.

All the functions of RBI (Reserve Bank of India) are controlled by BFS(Board for Financial Supervision), set up in November 1994. The main purpose of BFS is to oversee the Indian financial system, comprising commercial banks, state co-operative banks, All India financial institution (AIFI) and non-banking finance companies (NFFCs).

Main functions of RBI:

- Monetary authority: Oversee the monetary policy. Uses its monetary policy to control inflationary and deflationary situations in the economy.

- RBI acts as regulator and supervisor of the financial system: Provides wide functions to develop a sound banking system in the country. Protecting the interests of depositors and providing cost-effective banking services to the public.

- Foreign Exchange Control: Maintain the stability of the external value of the national currency-Indian rupee. Regulate the foreign exchange market in the country in terms of the Foreign Exchange Regulation Act (FERA), 1947.

- Currency Issuance: Issues currency notes and coins and puts them into circulation by exchanging or destroying them to give the public adequate supply.

- Government’s Banker: RBI acts as the banker to the central and state government by providing them with banking services for deposits, withdrawal and transfer of funds and managing public deposits.

- Banker to Banks: RBI maintains accounts of all scheduled (Appearing in the second schedule of the RBI Act) banks.

Tools of Monetary Control:

Cash Reserve Ratio (CRR): The cash reserve ratio is the cash that all Scheduled and non-scheduled banks are required to maintain with RBI as a certain percentage of their customer deposits and notes or their demand and time liabilities (DTL).

The raw cash of those banks is stored in a cash vault or in the form of deposits to the central banking authority.

A cut in CRR will bring down the call rates. An increase in CRR increases the call rate.

Statutory Liquidity Ratio (SLR): Statutory liquidity ratio refers to the money that all the scheduled and non-scheduled banks are required to maintain in the form of cash in hand, gold or government-approved securities (Bonds and shares of companies) before providing any credit to the customers.

Three objectives of SLR are; Restricts expansion of banks credit, Increase investment of banks in approved securities, and Ensure solvency of banks.

Bank Rate: The Bank rate is the rate of interest that the Central Banking Authority (RBI) charges to all commercial banks and other financial institutions on loanable resources and advances.

Commercial Banks

Commercial banks are the most common type of banks owned by the government, state or private organizations. Commercial banks include public sector banks, private sector banks, foreign banks and Regional Rural Banks. Public deposits are the main source of funds for these types of banks.

The commercial banking system in India is further divided into their sub-types.

- Public sector Banks – These banks are owned and operated by the Government or the Central Banking Authority – RBI. State Bank of India (SBI), Punjab National Bank (PNB), Allahabad Bank, and Bank of Baroda (BOB) are examples of public sector banks.

- Private sector Banks – These banks are privately owned and managed by a company. Axis Bank, ICICI Bank, and HDFC Bank are examples of Private sector Banks.

- Foreign Banks – These banks have branches in India and headquarters in foreign countries. Citibank, HSBC, and Standard Chartered are examples of Foreign Banks.

- Regional Rural Banks (RRBs) – Owned by the govt these banks provide services to rural and semi-urban areas.

Co-operative Banks

Co-operative Banks are organized under the state Co-operative Societies Acts 1912. They provide agriculture loans for farming and other agriculture-based activities.

- State Co-operative Banks – State Co-operative Banks are regulated by the RBI, State Govt and NABARD.

- Urban Co-operative Banks – Urban Co-operative Banks are the major Co-operative located in urban and semi-urban areas.

Small Finance Banks

As the name suggests these banks provide loans and financial assistance to small businesses, startups, small farmers and low-income individuals. These banks are governed by the Central Banking Authority of India. Here are examples of Small Finance Banks in India.

- AU Small Finance Bank Ltd.

- Capital Small Finance Bank Ltd.

- Utkarsh Small Finance Bank Ltd.

- Fincare Small Finance Bank Ltd.

- Ujjivan Small Finance Bank Ltd.

- Suryoday Small Finance Bank Ltd.

- Equitas Small Finance Bank Ltd.

- North East Small Finance Bank Ltd.

Specialized Banks

These types of banks are made for specific purposes. The purposes can be offering loans to small-scale industries, financial assistance to rural people and others.

EXIM banks, Small Industries Development Bank of India (SIDBI), and National Bank for Agricultural & Rural Development (NABARD) are examples of Specialized Banks.

Payments Banks

Payments Banks are the modern banking system in India that has been conceptualised by the central banking authority, RBI.

Payments banks are allowed to accept deposits up to Rs. 1,00,000/-. These banks offer services including Internet banking, mobile banking, ATM Cards, Debit cards, and others. Airtel Payments Bank, Jio Payments Bank, India Post Payments Bank, and Paytm Payments Bank are examples of Payments banks in India.

Scheduled Banks

Scheduled Banks operated under the 2nd Schedule of RBI Act 1934. A capital of Rs. 5 lakhs or more is needed for Scheduled Banks.

Non-scheduled Banks

Non-scheduled banks are local area banks registered under the Companies Act, of 1956.

Also Read – List of Banks in India- Headquarters and Taglines